A lot of would-be buyers have been playing a waiting game. There have been whispers on the wind that rates will come down further than they already have. Some folks who feel like they missed the hyper-low rates we saw in 2021 have been holding out.

In doing so, they might be missing out. First-time buyers aren’t building any equity as they sit on their hands. And even people who already own could be losing the chance to buy a home that suits them better.

Your mortgage team can help them get the best of both worlds: low rates and the ability to act today. A 3-2-1 buydown might be just the thing.

Helping borrowers understand buydowns (and their options)

The trick is that buydowns can be confusing for borrowers. Mortgages already tend to introduce a lot of jargon and math that people don’t interact with in their daily lives. Adding another layer of complexity can feel unwelcome.

You can help. All you need to do is simplify buydowns. Explain that they give the person a way to ease into their mortgage rate.

It might help to start with a 2-1 buydown as your example. This way, the borrower only has to think about three rates: their rate in the first year, the second, and every year after that.

You might give them this example. Say they get a 30-year fixed-rate mortgage at 6.25% with a 2-1 buydown. Explain that the “2” and “1” tell them how much their interest rate is reduced in each successive year.

As a result, their rate breaks down like this:

Once they have a good handle on what a 2-1 buydown means for them, you can introduce another layer — and a lower starting rate — with a 3-2-1 buydown. For that same example scenario, this would look like:

The lower rate in the early years can help borrowers envisioning acting now instead of waiting for rates to drop.

When to pitch 2-1 or 3-2-1 buydowns to borrowers

You can help your loan officers help their leads by highlighting some good buydown uses. The ability to start with a lower rate with a 2-1 or 3-2-1 buydown can be particularly helpful for:

- First-time buyers who are worried about managing a mortgage payment. A mortgage can be much more stressful than a rental agreement. First-time buyers want to know that they’re going to be able to handle this major financial obligation. If your loan officers help them find a good rate, then apply a buydown, it sets them up for success. They start with a lower rate, making monthly payments more affordable. Then, they can ease into their long-term rate year after year.

- Borrowers who got a low rate in 2019–2022. If you’ve got leads who scored a sub-4% rate, they might not be too excited about locking into today’s rates. With a buydown, you can get them closer to their current rate while still enabling them to move houses. This way, they can get into the home or neighborhood they want, then gradually move into their long-term rate.

- People who expect their income to increase. Many lenders pitch adjustable-rate mortgages to these folks, but some borrowers don’t like the uncertainty that comes with an ARM. With a buydown, they can take advantage of their increasing income levels while still knowing precisely what their monthly payment will be.

In each of these cases, a 2-1 or 3-2-1 mortgage buydown could provide incentive. Presenting this little-known way to get a lower starting rate should help your loan officers turn leads into closed loans.

Simplifying buydown math

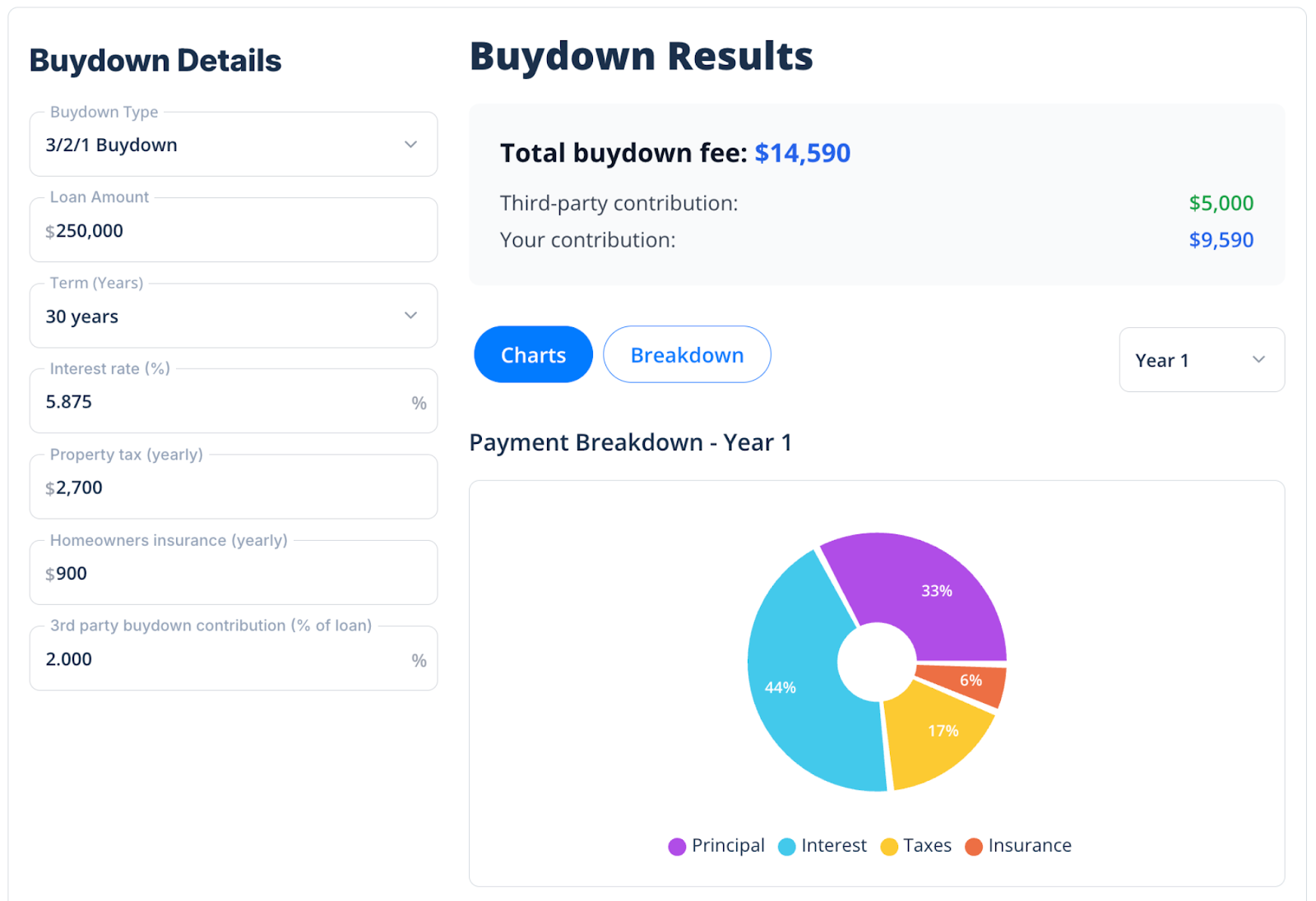

Once leads have a decent grasp on how a 2-1 and 3-2-1 mortgage buydown works, they’ll probably want to know how this tool could work for them. You can make it easy for them to find out with your own buydown calculator.

You have a couple of options here. You can maintain the calculator as an internal tool. When your loan officers meet with potential borrowers, they can pull up the calculator and use it to explore buydown options.

Alternatively, if you want to empower leads, you can host the buydown calculator on your website. If a borrower really wants it, they can find similar calculators on other sites. Having this tool readily available on your site helps you keep traffic on your own pages instead of diverting them to competitors.

In either instance, you don’t have to come up with the calculator on your own. We’ve already developed the code for the 3-2-1 buydown calculator. If you have someone on your team with development knowledge or you’ve worked with an external developer, they can help you deploy that calculator. Alternatively, our team here at BankingBridge can help.

We offer the bonus of connecting that buydown calculator with other tools you use, like your product pricing engine. This way, the calculator always pulls in the latest pricing information. That means your loan officers price scenarios for leads based on what’s actually available to them.

To explore getting a buydown calculator live for your team or on your website, we’re here. Book some time with our team at your earliest convenience.